This post is an opinion piece based on the following publications:

Stellantis discontinues hydrogen fuel cell programme (July ’25)

Toyota Provides Hydrogen Roadmap (March ’25)

The green hydrogen ambition and implementation gap (Jan ’25)

The Hydrogen Landscape in 2025

When I joined Ballard Power Systems in May of 2021, I stepped into the company that had been working on hydrogen fuel cells long before they were making headlines. On the production floor and in cross-functional meetings across engineering & ops, I saw buses and trucks being equipped with fuel cells that could run quietly, emit nothing but water, and refuel in minutes – a seemingly hermetic value proposition.

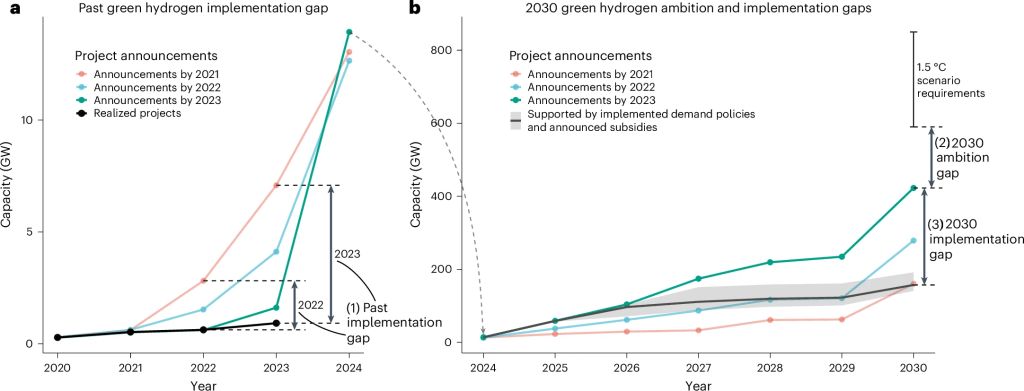

In spite of the promise of the technology, the challenges of implementation continue to linger – challenges that have caused retail investment to atrophy over the decades. Securing reliable hydrogen supply, building refuelling infrastructure, and convincing customers to commit to an industry with multiple false starts have made the path forward increasingly complex. Conversely, and rather optimistically, low-emissions hydrogen production is rapidly increasing year over year, driven by policy support and announced projects, with global production set to rise from less than 1 Mt in 2023 to potentially 49 Mt per annum by 2030. Installed electrolyzer capacity, a key technology for green hydrogen, doubled from 2022 to 1.4 GW by the end of 2023, and is projected to grow significantly by 2030. However – something the preceding issues potentially explain – only a small percentage of announced projects have secured final investment decisions (FIDs).

The Stellantis Retreat

In July 2025, Dutch automaker Stellantis announced it would discontinue its hydrogen fuel-cell van program. The vans simply couldn’t compete with battery-electric alternatives that were already cheaper, easier to change, and backed by more mature infrastructure. “The hydrogen market remains a niche segment, with no prospects of mid-term economic sustainability,” Jean-Philippe Imparato, chief operating officer for enlarged Europe, said in a statement. Stellantis’ retreat is less a death knell for hydrogen and more a reminder that it must be deployed selectively. For me, this echoed what I’d observed in the months following my time at Ballard – fuel cells excel in heavy-duty fleets and industrial use, but they struggle in segments where batteries already dominate.

The Implementation Gap

A recent Nature Energy study underscores this reality. Tracking 190 projects over three years (’21 – ’23), researchers found that only 7% of global green hydrogen capacity announcements were delivered on time. In practical terms, that means that out of the 7.1 gigawatts of electrolyzer capacity once promised for 2023, less than one gigawatt actually became operational. This shortfall reflects higher capital costs, uncertain demand, and the lack of long-term offtake agreements that would give developers the confidence to push forward. The study suggests that even as the pipeline of announced projects has nearly tripled to 422 gigawatts by 2030, most remain stuck at the feasibility or concept stage. Without stronger policies or meaningful carbon pricing, turning these ambitions into reality could require subsidies on the order of $1.3 trillion – several times higher than what governments have currently committed.

The Road Ahead

As hydrogen strides once again into an ostensibly defining decade, the strategic challenge will involve leveraging it’s uniqueness from a technological perspective as well as promoting its brand. From a regulatory point of view, policy certainty and subsidies will drive real progress. In the United States, the 45V tax credit’s extension through January 1, 2028, was a pivotal moment for green hydrogen providing a policy lifeline and injecting urgency into project planning. Still, analysts warn that up to 75% of announced projects may miss the credit’s eligibility timeline, potentially undermining U.S. competitiveness against fast-moving markets like China. But economic pinch points remain. Even in hydrogen-rich Australia, many flagship projects have faltered. Although the Australian government recently committed AUS $814 million to one such initiative, widespread execution failures and investor caution highlight how ambition without feasibility can lead to stalemate. At the same time, shifts in strategy are narrowing focus to sectors where hydrogen delivers tangible value – like chemicals and steel – rather than consumer application.

Do you see hydrogen becoming a cornerstone of the clean energy transition, or do you think its role will remain limited to a handful of niche applications?

Let me know your thoughts! I’d love to hear how others are thinking about hydrogen’s role in the energy transition ahead.

Leave a comment